.svg)

Q4 2025 Commercial Mortgage Market Update

2025 ended the way it started: with uncertainty doing most of the heavy lifting. Between a choppy macroeconomic backdrop, a Canadian economy that continued to feel like it was running uphill, and a real estate market still working through the post 2022 repricing, the lending market spent most of the year oscillating between caution and opportunism.

The difference by Q4 is that credit committees had largely stopped debating whether to lend and refocused on what they were willing to lend on. Across 2025, we saw a clear return to fundamentals: durable cash flow, sensible leverage, well located properties, and sponsorship strength that can survive delays (and, increasingly, bureaucracy). Pricing moved less than sentiment, but in our view the real story this year was not the direction of rates, it was the tightening of “approval standards” for anything perceived as transitional, speculative, or dependent on optimistic exit assumptions.

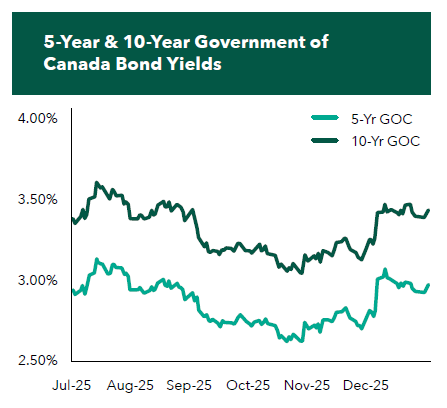

The late year theme was the one we kept circling back to all year, Canada and the U.S. are not moving in lockstep. In December, the U.S. Federal Reserve cut rates while the Bank of Canada held. The result was not a gentle drift lower in term borrowing costs. Bond yields shot up higher immediately putting further pressure on refinancing and acquisition activity.

If there is one takeaway heading into 2026, it is that borrowers will continue to live in a world where policy headlines matter, but bond markets matter more. Deals are still getting done. They just need to be built on today’s absorption, today’s cap rates, and today’s underwriting.

IPP Demand Remains Strong

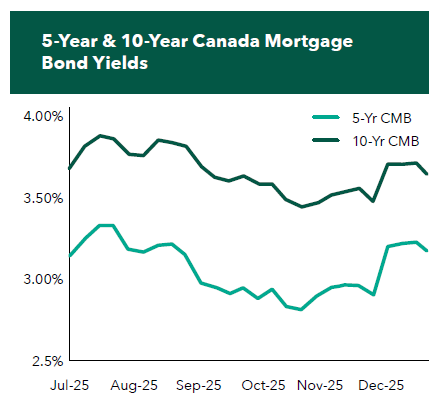

Focusing in on income producing properties, demand remained strong. Lenders continued to compete for high quality industrial, necessity retail, and conventional multifamily, and pricing for best-in class assets stayed attractive relative to everything else on the menu. That said, bond volatility made execution harder. Bond yield increases changes borrower math quickly, and it stretches timelines when lenders have to keep re-running the numbers.

Office is still the sector where lender selectivity is still felt the most. At the risk of sounding repetitive, office is not back, but it is also not a full stop anymore. Well leased Class A buildings in Toronto, Montréal, and Vancouver can still attract aggressive lender terms, especially where the sponsor is strong, and the capex plan is clear.

CMHC Update

For CMHC construction financing, if late 2024 was the year the market got introduced to rental achievement holdbacks again, 2025 was the year everyone had to actually finance around them.

Key CMHC themes we observed through 2025:

• Rental achievement holdbacks kept evolving: MLI Market loosened up on automatic holdbacks, while MLI Select continued to carry a more subjective approach until late November, where CMHC loosened the restriction to 85% LTC (subject to a cap of 95% LTV and 1.20x for standard multifamily).

• Energy efficiency and points math moved again: Updates to MLI Select energy efficiency parameters continued to affect design, documentation, and the economics of qualifying for the leverage and premium outcomes borrowers are targeting.

• Allocation pressure is real: The allocation rule change announced in September, with syndication flexibility ending by April 2026, is likely to keep upward pressure on insured loan pricing.

More developers continued to underwrite conventional construction to CMHC takeout parameters, including MLI Select take-outs, to avoid early process risk and keep timelines moving. In many cases, the trade has been simple, pay a bit more for money up front, save time, and land at similar net leverage, however with the rental achievement and energy efficiency changes, some projects may have the math shift back towards using MLI Select from the onset.

The CMHC Affordable Housing Program (“AHP”) was a little known and short-lived program that has now gone by the wayside with the advent of the new Build Canada Homes program that has been launched which although runs separately from CMHC financing, will incorporate many aspects of the former AHP program and have a somewhat similar process to the ACLP program. We continue to monitor the program for updates and will be assisting our developer clients on the approval process to access the attractive financing available from the Federal government.

Condo and Land Financing Still a Challenge

Condo development finance was still about price discovery in 2025. Fewer lenders were willing to get involved, even with presales, and the lenders that stayed active generally required higher hard presale thresholds, specifically with increasing scrutiny on presales with mortgage pre-approvals and significant purchaser deposits. Inventory financing remained available, but it was more selective, with lower leverage, and wider spreads. Land financing remained scarce. Extensions were possible, but typically with meaningful paydowns to align with today’s values.

OSFI Commercial Lending Proposal

OSFI published a proposal in November that is worth keeping an eye on. The regulator is looking at easing capital rules for certain corporate and real estate loans, with the stated goal of better aligning capital requirements with actual risk and freeing up bank balance sheets to extend credit and support growth. The key points were straightforward. OSFI opened a 90-day public consultation on changes to capital requirements for credit risk. The proposal includes lower risk weightings for loans to small and mid sized businesses, and for certain low rise residential real estate projects that OSFI views as relatively low risk. If adopted, banks would need to hold less capital against those loans. This is not in force yet, but any shift in capital treatment has a direct line to bank credit appetite and pricing.

Conclusion

As 2025 comes to a close, we look back on a year marked by a continued shift in how lenders and borrowers approach risk. The market is more constructive than it was a year ago, but it is also more disciplined. As we look forward to 2026, we anticipate a year that is built on cautious optimism that the worst is over. Market sentiment is that 2026 is likely not a breakout year, but potentially one more of stability and limited recovery. The Canada U.S. divergence is likely to remain part of the backdrop, and as long as that is the case, borrowers should assume bond yields will stay capable of surprising them. Keep leverage sensible, build in cushion, and lock when the deal works.

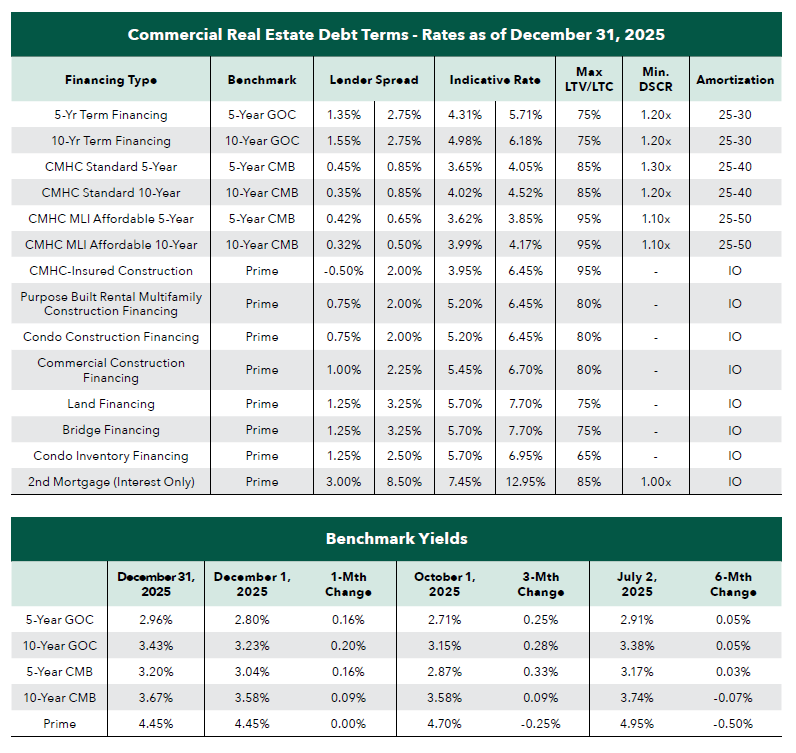

Selected Commercial Debt Terms and Benchmark Yields

Sign up for our newsletter

.svg)

.svg)